More Cities Lean Buyer-Friendly as Seller Momentum Softens in Phoenix, Arizona

- Brad Daniels

- 3 days ago

- 5 min read

The Greater Phoenix housing market continues to show subtle yet noticeable movement toward buyers, though overall conditions remain relatively stable amid the broader economy's volatility.

This week, the number of cities moving in a direction favorable to buyers held steady at 9, unchanged from last week. Meanwhile, 8 cities shifted in favor of sellers, with 1 city remaining unchanged. While the changes are still modest overall, the single-family detached market has once again edged slightly more in favor of buyers over the past month.

Two cities stood out most on the seller side this week: Surprise and Maricopa, both posted the largest percentage moves benefiting sellers, suggesting demand remains resilient in some of the more affordability-driven areas of the Valley.

On the other hand, Queen Creek and Paradise Valley led the movement toward buyers, continuing a trend we’ve seen recently where higher price points and increased inventory are giving buyers more negotiating leverage in certain luxury and move-up markets.

The average Cromford Market Index (CMI)* declined another 1.0% this week. That’s a more notable softening than last week’s modest 0.3% decline and signals that sellers are continuing to lose a bit of leverage as inventory gradually builds and buyers remain payment-sensitive.

Current market breakdown across the 18 major cities:

8 cities are currently in a seller’s market

4 cities are balanced

6 cities are in a buyer’s market

Even with the slight shift toward buyers, the market overall remains far more stable than many expected, given mortgage rate volatility, inflation concerns, and broader economic uncertainty. Most of the weekly changes remain relatively small, reinforcing that this is still a transitioning market rather than a sharply declining one.

For buyers, opportunities are slowly improving with more inventory, longer market times in some areas, and increased negotiating flexibility. For sellers, pricing strategy and presentation remain critical as buyers continue to be selective and highly payment-conscious.

Hotter Inflation, Higher Uncertainty: What It Means for Housing & Rates

Oh my! That April CPI! Inflation surged on higher energy prices, which affect far more than just gasoline and jet fuel (airline tickets, fertilizer, etc.). So far, the housing market is showing resilience, but there is little doubt that higher mortgage rates are keeping spring/summer transaction volumes more muted than they would be otherwise.

BLS: Economy added 115K jobs in April. While better than expected, April’s job growth was still modest. Over the last 12 months, only 251K net new jobs were created. The unemployment rate was steady at 4.3%. Meanwhile, the negative revisions continue: February’s original -92K number ended up at -156K after two revisions. [BLS]

Just look at the volatility of the BLS’ monthly jobs numbers! It looks like a Bitcoin price graph! Meanwhile, ADP’s monthly data has shown a clear — and fairly smooth — acceleration in job growth in 2026.

April CPI, oh my! We knew it was coming, and it finally arrived. Headline CPI (Consumer Price Index = inflation for you and me) jumped to +3.8% year-over-year in April from +3.3% YoY in March. And “Core” CPI (which excludes food & fuel prices) rose to +2.8% in April from +2.6% YoY in March. The main driver was higher energy prices (thanks to the US/Iran conflict), but shelter (housing) costs also jumped due to an accounting anomaly that should disappear next month.

After the scorching April CPI (and PPI) reports, the likelihood of a Fed rate cut during the remainder of 2026 dropped to zero. In fact, the market is now assigning a 30% probability that rates will be 25 basis points HIGHER than they are today by year-end.

Kevin Warsh confirmed as new Fed Chair by Senate. His confirmation hearings were contentious, focusing on: 1) his and the Fed’s independence given that he is President Trump’s appointee, and 2) his considerable individual and family wealth. Few questioned his qualifications.

Mr. Warsh inherits a deeply divided Fed. He will remain under considerable pressure from President Trump to cut rates, but inflation is resurgent, and the job market is (at least superficially) strong. While the Fed Chair’s voice can be highly persuasive in crafting a consensus view, he’s only got one vote.

Bond and Mortgage Market

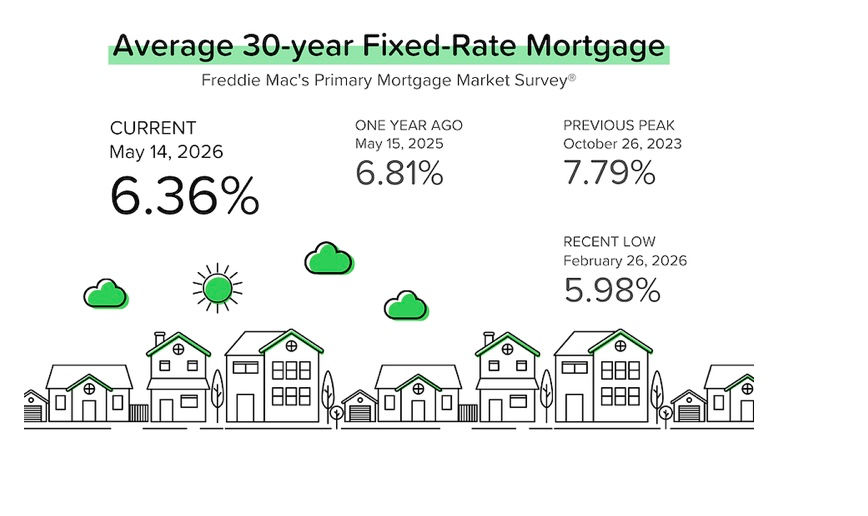

According to Freddie Mac’s weekly PMMS survey, average mortgage rates were roughly flat week-over-week. But given the bond market’s reaction to the scary April CPI figures, market mortgage rates are already moving higher. The market is still pricing in ZERO Fed rate cuts for the remainder of 2026. In fact, the market is beginning to price in some probability of rate HIKES towards the end of the year.

Note: The Fed Funds Rate policy range is currently 3.50–3.75%. The probabilities below come from the CME Group website and are implied from the Fed Funds Rate futures market.

• June 17 FOMC Meeting: This will be Kevin Warsh’s first meeting as the new Fed Chairman. 99% probability that the Fed Funds Rate will be kept at 3.50–3.75% (was 94% last week).

• July 29 FOMC Meeting: 99% probability that the Fed Funds Rate will be kept at 3.50–3.75% (was 88% last week).

• September 16 FOMC Meeting. 88% probability that the Fed Funds Rate will be kept at 3.50–3.75%. An 11% probability that rates will be 25 basis points HIGHER than they are today.

• No rate cuts in 2026? If I look way out to the last FOMC meeting of the year (Dec 9), the market is pricing in a 62% probability (was 72% last week) that the Fed Funds Rate will be exactly where it is today. Additionally, the market is now pricing in a 37% probability that rates will be at least 25 basis points (and maybe 50 basis points) higher by year-end.

Market in a Minute

Housing:

The Greater Phoenix single-family market continued a gradual shift toward buyers, with the average CMI* declining 1.0% over the past week — a larger change than the 0.3% decline we saw the week prior.

Mortgage rates moved higher this past week, briefly reaching their highest levels in over a month as inflation concerns and rising Treasury yields continued to pressure the bond market.

Of the 18 major cities tracked, 8 remain seller’s markets, 4 are balanced, and 6 are buyer’s markets, with Queen Creek and Paradise Valley showing the strongest movement favoring buyers.

Economy

April inflation came in hotter than expected, with CPI rising to 3.8% year-over-year as higher energy prices continued to ripple through the economy, impacting everything from transportation to consumer goods.

The U.S. economy added 115,000 jobs in April while unemployment held steady at 4.3%, though ongoing downward revisions to prior months continue to paint a mixed picture of the labor market.

Markets are now pricing in virtually no Federal Reserve rate cuts for the remainder of 2026, with some analysts beginning to anticipate the possibility of rate hikes later this year if inflation remains elevated.

Weather

☀️ Arizona weather doesn’t get much better than this.

With cooler temperatures and plenty of sunshine in the forecast, it’s the perfect week to get outside and enjoy everything the Valley has to offer—whether that’s hiking, golfing, relaxing by the pool, or exploring your favorite local spots.

If you’ve been thinking about making a move, this is also a great reminder of why so many people love calling Arizona home. 🌵

Take advantage of this beautiful weather and enjoy the week ahead! Direct: 602-679-1025 | brad@homeselleraz.com | www.relocatetoaz.com

Comments