Quiet Strength: Phoenix, AZ Real Estate Remains Steady Amid Uncertainty

- Brad Daniels

- 3 days ago

- 5 min read

Quiet Strength: Phoenix Real Estate Remains Steady Amid Uncertainty

While headlines continue to highlight economic uncertainty, the Greater Phoenix housing market is telling a very different story—one of consistency, balance, and subtle movement.

Over the past few weeks, we’ve seen very little change in overall market direction. The number of cities trending in favor of buyers remains at six, unchanged from the prior two weeks. Meanwhile, 12 cities are still leaning toward sellers, keeping the overall single-family detached market gently in favor of sellers.

That said, the shifts we are seeing continue to follow familiar patterns. Goodyear, Tempe, Maricopa, and Fountain Hills are once again showing the strongest momentum toward sellers, indicating continued demand and competitive conditions in those areas. On the flip side, Cave Creek and Gilbert are continuing to shift in favor of buyers, offering a bit more opportunity and negotiating room.

The Cromford® Market Index (CMI)* also reflects this steady pace. The average CMI rose 3.3% this past week—slightly stronger than last week’s 2.8% increase—showing modest but continued improvement for sellers without any dramatic swings.

Breaking it down further:

10 cities are currently in a seller’s market

2 cities are balanced

6 cities are in a buyer’s market

It’s worth noting that even within the seller’s markets, not all are created equal. Three of those ten are considered weak seller’s markets, with CMIs below 120—meaning buyers may still find opportunities even in areas that technically favor sellers.

The big picture? Not much has changed—and that’s actually a good thing.

In a time when financial markets, global events, and economic indicators can feel unpredictable, the Greater Phoenix housing market remains stable. Inventory, demand, and pricing are all moving in a measured, manageable way.

For buyers, that means opportunities still exist—especially in select cities where conditions are softening. For sellers, it means the market remains supportive, but strategy, pricing, and presentation matter more than ever.

In many ways, our local real estate market continues to be exactly what people are looking for right now: steady, reliable, and calm amid everything else.

*Cromford Market Index™ is a value that provides a short-term forecast for the balance of the market. It is derived from the trends in pending, active, and sold listings compared with historical data over the previous four years. Values below 100 indicate a buyer's market, while values above 100 indicate a seller's market. A value of 100 indicates a balanced market.

A Mixed Economic Picture: Strong Jobs Report, But Lingering Concerns

Threats, rescue missions, an ultimatum, and a ceasefire. The situation in the Middle East remains fragile and unpredictable. But back home, a stronger-than-expected jobs report contrasted with other signs of a cooling labor market.

Strong Jobs Report, but Questions Remain

March job growth came in well above estimates, according to the latest report from the Bureau of Labor Statistics. The economy added 178,000 jobs, well above forecasts of just 60,000. The unemployment rate also edged down from 4.4% to 4.3%.

What’s the bottom line? At first glance, this looks like a strong report. But other data suggest a more mixed picture. Reports from ADP and Revelio Labs showed smaller job gains (62,000 and 19,400, respectively), well below the BLS figure.

Revisions have also made the BLS data more volatile. For example, January job gains were revised higher, while February showed a larger loss. Over the past year, monthly results have frequently swung between gains and losses. All in all, the headline number doesn’t tell the whole story.

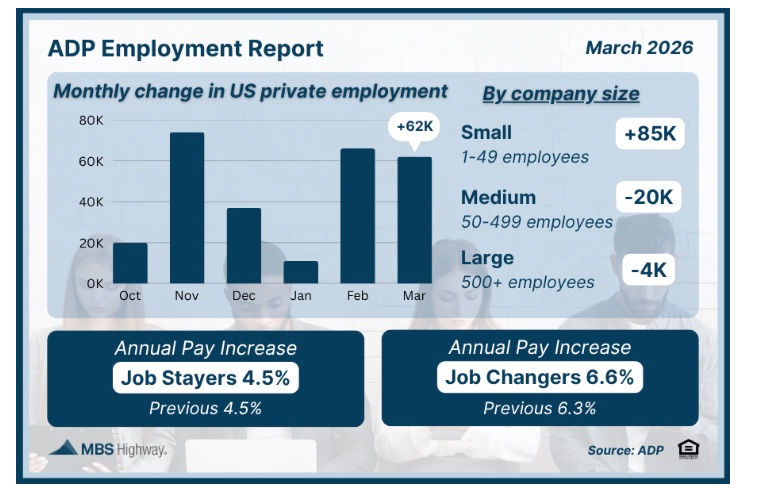

ADP Jobs Data Sends Mixed Signals

Looking closer at private-sector hiring, ADP data adds more context on where growth is occurring. Private employers added 62,000 jobs in March, beating forecasts of 40,000. But the headline masks important differences across company size and sector.

All the job growth came from small businesses, which added 85,000 positions. In contrast, medium-sized companies cut 20,000 jobs, and large employers trimmed 4,000.

What’s the bottom line? According to ADP Chief Economist Dr. Nela Richardson, overall hiring is steady but concentrated in a few areas. Much of the growth is coming from education and health services, industries that tend to be more stable and less sensitive to economic shifts.

At the same time, the payoff for switching jobs is shrinking. Workers who change jobs are still seeing faster wage growth (6.6%) than those who stay put (4.5%), but the gap has narrowed compared to recent years. In other words, the job market is becoming less competitive overall.

Bond and Mortgage Market

Since peaking around 6.65% on March 27, average 30-year mortgage rates have been trending lower. Now, with the 2-week ceasefire supposedly in place, and ships transiting the Straits of Hormuz again, that downtrend in mortgage rates could continue.

Note: The Fed Funds Rate policy range is currently 3.50–3.75%. The probabilities below come from the CME Group website and are implied from the Fed Funds Rate futures market.

• April 29 FOMC Meeting: 98% probability that the Fed Funds Rate target range is kept at 3.50–3.75% (was 97% last week). And…a 2% probability (was 3% a week ago) that the Fed will raise rates 25 basis points.

• June 17 FOMC Meeting: 94% probability that the Fed Funds Rate will be kept at 3.50–3.75% (unchanged from last week). So, no rate cut at either the April or June meeting.

• No rate cut in 2026? If I look way out to the last FOMC meeting of the year (Dec 9), the market is pricing in a 73% probability (same as last week) that the Fed Funds Rate will be exactly where it is today. In other words, the market continues to price in NO rate cuts for the entirety of 2026. There is only a 14% probability that rates will be 25 basis points below current levels, and a 12% probability that they will be 25 basis points above current levels.

The Market in a Minute

Housing:

The overall market continues to lean gently in favor of sellers, with little change week over week

12 cities favor sellers while 6 favor buyers, showing steady and balanced conditions across the Valley

Some seller markets remain weak (CMI under 120), creating opportunities for buyers in select areas

Economy:

Job growth came in stronger than expected, but hiring is concentrated in more stable sectors like education and healthcare

The labor market is showing signs of cooling, with the wage gap between job switchers and stayers continuing to narrow

Mortgage rates have been trending slightly downward, while markets still expect no Fed rate cuts through the remainder of 2026

Relocating to or from Arizona? I would love to help. Reach out to Brad at 602-679-1025

Have a great week!

Comments